IIFT International Business and Management Review Journal

Search

Search

Subodh, K. Juikar1  and Sampada S. Juikar2

and Sampada S. Juikar2

1Indian Institute of Packaging, Mumbai, Maharashtra, India

2Vivekanand Education Society, Mumbai, Maharashtra, India

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-NonCommercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

The continual economic evolution in the world has generated fears about the depletion of natural resources. In recent years, the industries have focused on the ‘green business’ concept to prioritise a sustainable environment by minimising their effects on the environment. Thus, the industry is offering environmentally friendly products or services, reducing the carbon footprint, to support green initiatives through local partnerships and philanthropy. This article explores the correlation between sustainability and corporate social responsibility (CSR), highlights the different approaches employed by the industry to accomplish these responsibilities, and appraises the development in the Southeast Asian region. Although Southeast Asia has opted for various CSR initiatives and has been engaged in environmental sustainability drives, the effect is far too minimal in most of the countries. Regardless of the increasing trend of global interest in adopting CSR among businesses, as of date, the share of businesses adopting CSR is still relatively very low. The CSR journey of Southeast Asia is marked by strong community engagement, government influence and emerging regulatory frameworks. The region has to face both challenges and avail an opportunity to redefine CSR within its own socio-economic context.

Sustainability, modern business, economic evaluation, corporate social responsibility, Southeast Asia,

Introduction

The concept of ‘Green Business’ is not new to the exponentially growing industries world over. It roused during the 20th century due to increasing concern about environmental issues like depletion of natural resources due to their exhaustive usage.

In today’s globalised economy, sustainability and corporate social responsibility (CSR) the green business has emerged as non-negotiable essentials for business. Stakeholders ranging from customers and employees to investors and regulators demand that companies should not only deliver profits but also be sustainable.

Today, businesses are no longer judged solely by their financial performance, but they are being judged by their contributions to the environment, and thus, the sustainable business practices form the backbone of long-term value creation. From reducing environmental harm to supporting communities and upholding ethical governance, CSR initiatives align corporate actions with broader societal needs (Aghelie, 2017; Aithal, 2019; Purwandani & Michaud, 2021; Rai & Jambhulkar, 2018; Singh & Thakar, 2018; Utting, 2000).

This study focuses on the adoption and implementation of CSR and sustainability practices with an emphasis on Southeast Asia. The role of CSR in advancing sustainability within modern business, vis-à-vis the current state of CSR adoption in Southeast Asian countries, and to identify the advantages of integrating CSR into business strategies is studied. Further, the comparison of CSR practices in Southeast Asia vis-à-vis those in developed countries, by highlighting the differences, gaps and limitations of CSR adoption and in Southeast Asia, with emphasis on fiscal and tax-related barriers, are discussed. The recommendations on the strategies for overcoming implementation challenges and aligning CSR with global sustainability standards are also provided to bridge the gaps and offer the region the opportunities to redefine CSR.

Today, there is a need to understand how companies are engaged in sustainable development, their impact on financial performance, and how they navigate diverse institutional, cultural and political contexts. This study will help to identify key factors shaping practices, explore the shift from obligation to strategic tool, and inform policies for promoting more effective and impactful initiatives, especially as a response to increasing globalisation and development challenges. This will also help the companies build stronger brands, improve customer loyalty, attract and retain talent, and foster long-term sustainability. Understanding CSR issues will also enable individuals to help businesses to integrate ethical and environmental considerations into their strategies. The study will also propose strategies for overcoming implementation challenges and aligning CSR with global sustainability standards.

The Green Business Practices

The terms ‘green economy’ or ‘green business’ may be defined as an economy or business which minimises its negative impacts on the environment while improving the welfare of society by different means. The term ‘green’ is normally used for an action towards a sustainable environment. It highlights the environmental impact arising from any organisation and environmental policies of governments, national and international environmental regulations, and competitive pressures.

There are various terms being used for referring to the concept of ‘green business’. These are sustainopreneurship, ecoentrepreneurship, environmental entrepreneurship, ecological entrepreneurship, ecopreneurship, sustainable entrepreneurship and enviropreneurship. All these phrases refer to entrepreneurs and smaller businesses willing to decrease their environmental impact and improve their activities towards green principles like sustainability and environmental friendliness. It is also defined as ‘creating value through ecological principles’ and ‘entrepreneurship through an environmental lens’. Today, a green business is a way to accomplish green growth. It is a development that emphasises confirming the sustainability of the environment and, at the same time, promotes economic growth (Aithal, 2019; Purwandani & Michaud, 2021).

The reason behind adopting green business practices in many developing countries like India varies. Sometimes it is required by customers or by regional governments. In some cases, the organisation may think of it as an investment opportunity. The organisation may implement it due to the self-motivation of the stockholders or due to pressure from the community. Some organisations implement it for improving their brand image in the public. Generally, larger organisations are more familiar with the approach, as they acquire more efficient management functionality and discipline (Aghelie, 2017; .png) ekanavi

ekanavi.png) ius et al., 2014; Purwandani & Michaud, 2021; Rai & Jambhulkar, 2018; Singh & Thakar, 2018).

ius et al., 2014; Purwandani & Michaud, 2021; Rai & Jambhulkar, 2018; Singh & Thakar, 2018).

The Role of CSR in Advancing Sustainability

CSR refers to a company’s commitment to manage its operations ethically, contributing to economic development while improving the quality of life for its workforce, their families, the local community and society at large. Sustainability, in this context, focuses on the environmental dimension of CSR, ensuring that resources are used responsibly to support long-term planetary health. Together, these approaches ensure that businesses are accountable for their impacts and are proactive in addressing challenges such as climate change and carbon emissions, biodiversity loss and habitat degradation, water and air pollution and social inequalities and labour exploitation (European Commission, 2019; International Organization for Standardization [ISO], 2010; United Nations, 2015; United Nations Global Compact, n.d.; US Environmental Protection Agency, n.d.; World Bank, 2021).

Thus, by aligning business practices with CSR principles, organisations can minimise harm and enhance their environmental and social footprints, strengthen community trust and stakeholder relationships, meet legal and ethical obligations, and drive innovation and competitiveness in a values-based market (Elkington, 1994; Ellen MacArthur Foundation, 2021; Harvard Business Review, 2016; ISO, 2010).

Core Strategies for Responsible and Sustainable Business

Sustainable business practices often lead to improved efficiency and reduced costs, which can directly impact an organisation’s profile. For example, the implementation of energy-efficient technologies can lower utility expenses, while sustainable supply chain practices can reduce waste and improve operational efficiencies. The following are some of the core strategies for businesses to be ‘Responsible and Sustainable’.

Environmental Stewardship

It is about protecting and responsibly using the natural environment through sustainable practices and conservation efforts, and ensuring the long-term healthy ecosystems and the well-being of future generations. It involves making choices and taking actions that minimise negative impacts and promote a healthy environment. The organisations involved in CSR activities can help in reducing the environmental burden of their business in different ways. For example, the business may adopt energy-efficient processes and technologies, or substitute renewable energy in the processes wherever feasible, or reduce waste generation using circular economy models, or may encourage the use of sustainable packaging (Ellen MacArthur Foundation, 2021; Global Reporting Initiative, 2021; Patagonia, 2023; World Bank, 2021).

Ethical Supply Chains

An ethical supply chain is a system where businesses prioritise fair labour practices, environmental sustainability and human rights throughout their entire supply chain, from sourcing raw materials to delivering finished products. This approach involves establishing strong relationships with suppliers, monitoring their compliance with ethical standards, and addressing any issues that arise. A sustainable business ensures that its entire value chain, from raw materials to product delivery, adheres to ethical and environmental standards. This can be done by evaluating the suppliers for environmental and labour compliance, or by improving transportation to reduce the carbon footprint, or by encouraging local and fair-trade sourcing (Global Reporting Initiative, 2021; ISO, 2010; United Nations, 2015; United Nations Global Compact, n.d.).

Community and Social Engagement

The organisation can achieve this by actively participating in communities and society, and by fostering a sense of belonging, to work together for resolving common issues. It encompasses various forms of participation, including volunteering, attending community events, and joining clubs or businesses engaged in CSR activities are supporting local communities in different ways, like providing education to needy students, providing facilities for improving the health of the underprivileged sectors, and infrastructure, or by promoting equity and diversity, or by strengthening underrepresented groups, and by supporting fair wages and so on (Elkington, 1994; ISO, 2010; United Nations, 2015).

Transparent Governance and Reporting

Transparent governance and reporting involve making information about government and corporate actions readily accessible to the public, promoting accountability and public trust. It is a key element of good governance and helps prevent corruption by allowing citizens to monitor how resources are used and hold officials accountable. The sustainability performance must be measurable and transparent. This can be done by the implementation of various CSR activities, which will help in adopting reporting standards on environmental, social and governance (ESG), and obligating to third-party audits/certifications like ISO 14001, and ensuring accountability through stakeholder communication (Global Reporting Initiative, 2021; ISO, 2010; United Nations Global Compact, n.d.).

Employee Involvement and Workplace Well-being

Employee involvement and workplace well-being are intertwined, impacting both employee health and organisational success. Prioritising employee welfare nurtures a more engaged and productive workforce and provides benefits like improved satisfaction levels and enhanced work culture. Organisations internal sustainability thrives on a responsible culture. The CSR strategies focus on various aspects, like employee training and involvement in green initiatives, work–life balance, workplace health, ethical leadership and open dialogue (Asian Development Bank [ADB], 2022; Harvard Business Review, 2016; United Nations Global Compact, n.d.).

Environmental Governance and CSR Progress in Southeast Asia

For implementing CSR activities and fostering sustainable growth in Southeast Asia, the industry witnesses both challenges and opportunities. The Southeast Asia region faces critical environmental issues, including pollution, deforestation and climate risks, which are often intensified by rapid industrialisation (United Nations Global Compact, n.d.; World Bank, 2021). However, in recent years, those organisations that have taken CSR initiatives at the regional and national levels are progressing notably. The steps taken by different countries for improving regional and national sustainability are discussed below.

Government Initiatives

Policies such as Malaysia’s Green technology master plan and Thailand’s Bio-Circular-Green (BCG) Economy Model promote responsible business transformation. These plans integrate sustainability goals with national economic development (ADB, 2022; United Nations Economic and Social Commission for Asia and the Pacific [UNESCAP], 2020).

Corporate Engagement

Increasingly, companies in Vietnam, Indonesia and the Philippines are adopting environmental impact assessments and sustainability reporting as standard practices. Green financing, ESG benchmarks and CSR disclosures are gaining traction (IKEA, 2023; Unilever, 2022; World Bank, 2021).

Regional Cooperation

The countries from the Association of Southeast Asian Nations (ASEAN) are working together through frameworks like the ASEAN Agreement on Transboundary Haze Pollution, addressing shared environmental challenges through joint governance (ASEAN, 2021; UNESCAP, 2020).

Civil Society and Non-governmental Organisations (NGOs)

NGOs and watchdog groups are playing a pivotal role in driving transparency, pressuring companies and governments alike to meet sustainability standards and honour CSR commitments (ASEAN, 2021; UNESCAP, 2020).

Benefits of Integrating Sustainability and CSR in Business

Performing CSR activities is an excellent way to exhibit an organisation’s attitude on the environment, economy and society. This self-regulating business model helps organisations be socially accountable to themselves, their stakeholders and the public. By practising CSR, organisations can become conscious of the kind of impact they have on all aspects of society. The following are some of the important benefits which can avail by the organisations participating in sustainability and CSR in their business.

Reputational Strength and Market Positioning

Organisations that demonstrate genuine responsibility build strong reputations. Today, in competitive markets, there are increased customer loyalty concept among the younger generation and socially aware consumers. CSR initiatives help differentiate brands (Harvard Business Review, 2016; Patagonia, 2023).

Financial Resilience and Investment Opportunities

Green businesses are increasingly attracting green ESG-focused investors. The CSR alignment also opens access to government incentives, subsidies and international green financing options (ADB, 2022; Harvard Business Review, 2016; IKEA, 2023).

Operational Efficiency and Risk Mitigation

Energy and resource-efficient operations reduce costs and buffer against regulatory risks, supply chain disruptions and environmental liabilities (Elkington, 1994; European Commission, 2019).

Long-term Innovation and Growth

CSR nurtures a culture of innovation. From eco-friendly product design to clean technology and digital transparency tools, sustainable companies often lead in new product and service development (Ellen MacArthur Foundation, 2021; Patagonia, 2023).

Contribution to Global Goals

CSR-driven businesses contribute meaningfully to the United Nations Sustainable Development Goals (SDGs), especially those focusing on climate action, responsible consumption, decent work and inclusive economic growth (United Nations, 2015).

Limitations of CSR in Southeast Asia on Tax and Fiscal Pressures

Despite the growing importance of sustainability, businesses in Southeast Asia face significant fiscal and financial constraints that limit their CSR capacity. As given below, these limitations differ from those in developed economies and must be considered to understand the regional CSR landscape.

Overall, the tax and fiscal pressures create a structural limitation for CSR adoption in Southeast Asia. Unless governments strengthen fiscal incentives, simplify compliance for SMEs and integrate CSR spending into tax-deductible frameworks, CSR will remain concentrated among large corporations rather than being a widespread regional business practice (Nguyen et al., 2020; OECD, 2021; Yoshino et al., 2023).

Overcoming Challenges in CSR Implementation

Running a green business is indeed a challenging job. Many businesses have adopted CSR and other environmental policies. Many are engaged in corporate aid and taking measures to improve the impact of their business. However, the overall effects of these trends are far weaker in most developing countries (Aithal, 2019). Many large corporate organisations in Southeast Asia have their CSR policies; however, the implementation levels vary significantly in these countries (Putra et al., 2024). Despite growing momentum, companies may face obstacles in the implementation of CSR in their businesses. This may include stakeholder resistance to change, high initial costs, resource constraints, complexity in global supply chains, regulatory complexity and so on (Aithal, 2019; Utting, 2000). Some of the solutions for overcoming the challenges include: access to low-interest loans, tax breaks and subsidies that support sustainable investments, starting with low-cost or high-impact areas allows manageable transitions, partnering with NGOs, academic institutions, and industry peers enhances knowledge and collective action and publishing regular CSR reports fosters trust and enables benchmarking progress (Global Reporting Initiative, 2021; Harvard Business Review, 2016; IKEA, 2023; UNESCAP, 2020; United Nations Global Compact, n.d.).

How Southeast Asia is Different from Others in CSR

Southeast Asia has unique characteristics compared to other regions. With respect to the regulatory and voluntary approaches, in Europe and North America, CSR is often market-driven and integrated voluntarily into business strategy, influenced by consumer and investor expectations (Matten & Moon, 2020), but in Southeast Asia, CSR adoption is more government-led. National frameworks such as Malaysia’s Green Technology Master Plan and Thailand’s BCG Model provide policy direction, but enforcement varies across countries (ASEAN Secretariat, 2023; OECD, 2022).

Also, Southeast Asia closely focuses on community development, philanthropy and social welfare, reflecting cultural values of collectivism and social responsibility (Chapple & Moon, 2005; Visser, 2016). By contrast, Western CSR emphasises environmental impact, corporate governance and transparency in global supply chains (Porter & Kramer, 2019).

The Southeast Asian economy relies heavily on SMEs, many of which struggle with financing and knowledge gaps to implement CSR (ADB, 2021). However, global multinationals usually have greater as discussed in the limitations (PricewaterhouseCoopers [PwC], 2023).

Nowadays, large ASEAN corporations are making significant progress in sustainability reporting and green finance, while smaller firms often treat CSR as charitable giving rather than as an integrated business strategy (UNESCAP, 2022); compared to Western economies, CSR has matured into long-term strategic commitments tied directly to profit models (Carroll, 2021). And regarding financing and investment, the global ESG investment market exceeds $35 trillion, while ASEAN’s remains relatively modest ($300 billion in 2022). This limits the scale of sustainable transformation in the region compared to Europe and North America (OECD, 2022; World Bank, 2023).

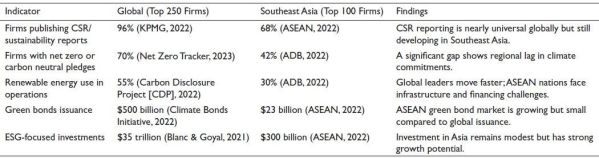

Thus, Southeast Asia’s CSR is highly dependent on the engagement of the community, the influence of the government and emerging regulatory frameworks. Though in global trends of CSR underscore market-driven transparency, the integration of advanced ESG and financing on a large scale (ASEAN Secretariat, 2023; ADB, 2021). Table 1 illustrates the comparative CSR and sustainability adoption trends across global corporations and Southeast Asia, showing levels of ESG reporting, renewable energy use and sustainability-linked investment.

There are significant differences in CSR adoption between global corporations and Southeast Asian firms (ASEAN Secretariat, 2023; OECD, 2021; PwC, 2023). The global corporations report an 85%–90% adoption rate, while Southeast Asian firms show 50%–60% (PwC, 2023; World Bank, 2023). This gap suggests that CSR remains more of a compliance-driven or reputational practice in Southeast Asia, rather than a deeply integrated business strategy (Carroll, 2021; Visser, 2016). The global business has achieved a 50%–60% renewable energy integration, while Southeast Asia lags at 15%–20% (ADB, 2021; OECD, 2021). This demonstrates limited investment capacity, weaker policy incentives and infrastructure constraints in the region (Nguyen et al., 2020). Over 70% of global firms have announced carbon neutrality targets, compared to only 30% in Southeast Asia (ASEAN Secretariat, 2023; World Bank, 2023). This reflects weaker enforcement of carbon neutrality in ASEAN economies (Porter & Kramer, 2019). The ESG-related investments in global firms account for 40%–45% of financing, while Southeast Asian firms are at just 10%–12% (Bloomberg Intelligence, 2023; OECD, 2021; PwC, 2023). This indicates underdeveloped green financial instruments in the region, limited availability of ESG bonds and weaker integration of sustainability into financial markets (ADB, 2021).

Table 1. Corporate Social Responsibility (CSR) and Sustainability Adoption Trends Across Global Corporations and Southeast Asia.

Note: ASEAN: Association of Southeast Asian Nations; ESG: Environmental, social and governance.

The comparison between global firms increasingly aligns with Global Reporting Initiative (GRI), Sustainability Accounting Standards Board (SASB) and Task Force on Climate-related Financial Disclosures (TCFD) standards, whereas Southeast Asian firms show inconsistent reporting practices (ASEAN-BAC, 2025; PwC, 2023). This reflects differences in regulatory frameworks and governance capacity (Matten & Moon, 2020).

It is seen that, while Southeast Asia is making progress in CSR adoption, the region lags significantly behind global counterparts in terms of renewable energy, carbon neutrality and ESG financing (OECD, 2021; Tesla, 2023; World Bank, 2023). The structural issues, such as fiscal pressures, weak regulatory incentives and fragmented reporting systems, remain major barriers (ADB, 2021; Nguyen et al., 2020). If Southeast Asia can strengthen policy support, tax incentives and financial instruments, the gap in CSR implementation could narrow significantly (ASEAN Secretariat, 2023; PwC, 2023). The following are some of the recommendations proposed by various researchers for businesses and policymakers in Southeast Asia.

Conclusion

Sustainable development emphasises and ensures environmental protection and, at the same time, promotes economic growth. Sustainability and CSR are no longer add-ons and are the foundation of the success of modern businesses. By embedding CSR into corporate strategy, companies not only future-proof their operations but also champion a vision of business as a force for good. From environmental protection to social equity, CSR strengthens businesses to lead with purpose, engage stakeholders and contribute to a more resilient and inclusive global economy. In this time of growing environmental and ethical awareness, organisations that walk the talk will define the future.

Today, running a green business is a challenging job in Southeast Asian countries. Many SMEs are struggling to overcome various barriers associated with green business. Despite the increasing wave of global enthusiasm for adopting CSR among businesses, the share of companies adopting CSR is still relatively very low. However, in the CSR journey of Southeast Asia, along with strong community engagement and government influence, there exists an emerging regulatory framework, but it differs from global CSR trends, which emphasise market-driven transparency and advanced ESG integration, along with large-scale financing. Bridging these gaps will offer the Southeast region both a challenge and an opportunity to redefine CSR within its own socio-economic context, and looking at the pace of technological development in Southeast Asian countries, it is opined that the green business concept will definitely be the need of businesses for promoting sustainable growth.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

ORCID iD

Subodh K. Juikar https://orcid.org/0009-0009-8736-9866

Aghelie, A. (2017). Exploring drivers and barriers to sustainability green business practices within small medium sized enterprises: Primary findings. International Journal of Business and Economic Development (IJBED), 5(1), 41–48.

Aithal, S. (2019). Challenges associated with running a green business in India and other developing countries. https://mpra.ub.uni-muenchen.de/95163/

ASEAN. (2021). ASEAN state of the environment report 2021. ASEAN Secretariat. https://environment.asean.org/

ASEAN. (2022). ASEAN state of the environment report 2021. ASEAN Secretariat. https://environment.asean.org/

ASEAN-BAC. (2025). CSR in ASEAN: From obligation to development strategy.

ASEAN Secretariat. (2023). ASEAN Sustainable Development Goals report 2023.

Asian Development Bank (ADB). (2021). ASEAN small and medium-sized enterprises and sustainability transition. ADB Publications.

ADB. (2022). Financing a green and inclusive recovery in Southeast Asia. https://www.adb.org/

Blanc, D., & Goyal, A. (2021). Latest edition of the Global Sustainable Investment Review confirms strong growth of ESG assets all over the world. Natixis CIB Green & Sustainable Hub. https://gsh.cib.natixis.com/our-center-of-expertise/articles/latest-edition-of-the-global-sustainable-investment-review-confirms-strong-growth-of-esg-assets-all-over-the-world

Bloomberg Intelligence. (2023). Global ESG market outlook. Bloomberg L.P.

Carbon Disclosure Project (CDP). (2022). Renewable energy and climate reporting. https://www.cdp.net/

Carroll, A. B. (2021). Corporate social responsibility: Perspectives on the CSR construct’s development and future. Business & Society, 60(6), 1256–1283.

Carroll, A. B., & Brown, J. (2018). The state of CSR in 21st-century business. Journal of Business Ethics, 152(2), 1–15.

ekanaviius, L., Bazyt.png) , R., & Dimonait, A. (2014). Green business: Challenges and practices. Ekonomika, 93(1), 74–88.

, R., & Dimonait, A. (2014). Green business: Challenges and practices. Ekonomika, 93(1), 74–88.

Chapple, W., & Moon, J. (2005). Corporate social responsibility (CSR) in Asia: A seven-country study of CSR web site reporting. Business & Society, 44(4), 415–441.

Climate Bonds Initiative. (2022). Global State of the Market Report 2022. https://www.climatebonds.net/files/documents/publications/Global-State-of-the-Market-Report-2022.pdf

Elkington, J. (1994). Towards the sustainable corporation: Win-win-win business strategies for sustainable development. California Management Review, 36(2), 90–100.

Ellen MacArthur Foundation. (2021). What is a circular economy? https://ellenmacarthurfoundation.org/topics/circular-economy-introduction/overview

European Commission. (2019). The European Green Deal. https://ec.europa.eu/info/publications/communication-european-green-deal_en

Global Reporting Initiative. (2021). Consolidated set of GRI sustainability reporting standards 2021. https://www.globalreporting.org/

Inter IKEA Systems B.V. (2023). IKEA Sustainability Report FY22 [PDF]. IKEA. https://www.ikea.com/global/en/images/ikea_sustainability_report_fy22_57c0217c71.pdf

International Organization for Standardization (ISO). (2010). ISO 26000:2010—Guidance on social responsibility. https://www.iso.org/iso-26000-social-responsibility.html

KPMG. (2022). Survey of sustainability reporting 2022. https://kpmg.com/xx/en/home/services/advisory/sustainability-services.html

Matten, D., & Moon, J. (2020). Reflections on the 20th anniversary of “Implicit and explicit CSR”. Journal of Business Ethics, 162, 485–499.

Net Zero Tracker. (2023). Net zero targets among world’s largest companies double, but credibility gaps undermine progress. https://zerotracker.net/insights/net-zero-targets-among-worlds-largest-companies-double-but-credibility-gaps-undermine-progress

Nguyen, T., Oxfam, & VEPR. (2020). Towards sustainable tax policies in the ASEAN region: The case of corporate tax incentives. Oxfam.

Organisation for Economic Co-operation and Development (OECD). (2021). Facilitating the green transition for ASEAN SMEs. OECD Publishing.

OECD. (2022). Southeast Asia economic outlook 2022: Financing sustainable recovery. OECD Publishing.

Patagonia. (2023). Environmental & social responsibility. https://www.patagonia.com/our-footprint/

Porter, M. E., & Kramer, M. R. (2019). Creating shared value: Redefining capitalism and the role of the corporation in society. Harvard Business Review, 97(1), 66–77.

PricewaterhouseCoopers (PwC). (2023). ESG reporting trends in ASEAN: Challenges and opportunities. PwC Southeast Asia.

Purwandani, J. A., & Michaud, G. (2021). What are the drivers and barriers for green business practice adoption for SMEs? Environment Systems and Decisions, 41(4), 577–593. https://doi.org/10.1007/s10669-021-09821-3

Putra, K. D. C., Wattanametha, P., Saputra, U. W. E., Widiantara, I. M., Elfarosa, K. V., & Rahmanu, I. W. E. D. (2024). A cross-country comparison of the corporate social responsibility orientation between Indonesia and Thailand: Do gender and culture matter? Asia Pacific Management and Business Application, 13(2), 145–166.

Rai, S., & Jambhulkar, S. (2018). An analytical study of green business practices in India with specific reference to selected Indian companies. International Journal in Management and Social Science, 6, 1–15.

Singh, M. D., & Thakar, G. D. (2018). Green manufacturing practices in SMES of India—A literature review. Industrial Engineering Journal, 11(3), 37–45.

Tesla. (2023). Impact report. https://www.tesla.com/impact

Unilever. (2022). Sustainable living plan and ESG performance. https://www.unilever.com/planet-and-society/

United Nations. (2015). Transforming our world: The 2030 Agenda for Sustainable Development. https://sdgs.un.org/2030agenda

United Nations Economic and Social Commission for Asia and the Pacific (UNESCAP). (2020). Green recovery pathways in Southeast Asia. https://www.unescap.org/

UNESCAP. (2022). Sustainability and CSR progress in ASEAN. UNESCAP Publications.

United Nations Global Compact. (n.d.). The ten principles of the UN Global Compact. https://www.unglobalcompact.org/what-is-gc/mission/principles

US Environmental Protection Agency. (n.d.). Sustainability. https://www.epa.gov/sustainability

Utting, P. (2000). Business responsibility for sustainable development (Geneva 2000 Occasional Paper No. 2). United Nations Research Institute for Social Development (UNRISD). https://hdl.handle.net/10419/148835

Visser, W. (2016). The evolution and revolution of corporate social responsibility. Social Responsibility Journal, 12(2), 190–207.

Whelan, T., & Fink, C. (2016, October 21). The comprehensive business case for sustainability. Harvard Business Review. https://hbr.org/2016/10/the-comprehensive-business-case-for-sustainability

World Bank. (2021). Southeast Asia: Regional climate risk profile. https://www.worldbank.org/

World Bank. (2023). Southeast Asia green growth and sustainable finance report 2023. World Bank Group.

Yoshino, N., Arifin, J., & Kimura, F. (2023). SMEs and carbon neutrality in ASEAN: The need to revisit strategies. Journal of Southeast Asian Economies, 40(2), 155–170.