IIFT International Business and Management Review Journal

Search

Search

1Department of Finance, Faculty of Management and Finance, University of Colombo, Sri Lanka

Creative Commons Non Commercial CC BY-NC: This article is distributed under the terms of the Creative Commons Attribution-Non Commercial 4.0 License (http://www.creativecommons.org/licenses/by-nc/4.0/) which permits non-Commercial use, reproduction and distribution of the work without further permission provided the original work is attributed.

The life insurance industry is a cornerstone of the Sri Lankan financial system, driving economic growth through capital mobilisation and liquidity creation. Despite its importance, Sri Lanka exhibits a notably low life insurance penetration rate compared to other Asian countries. This study investigates the critical factors influencing the purchase behaviour of life insurance among individuals in Sri Lanka, filling a gap in localised empirical research. The research adopts a quantitative approach, utilising the Theory of Planned Behaviour and the Theory of Reasoned Action as its theoretical framework. Primary data were collected via structured questionnaires from a sample of 391 individuals across all 9 provinces of Sri Lanka. The study examines six independent variables: insurance literacy, attitude, subjective norms, trust, risk perception and perceived behavioural control, with purchase intention serving as the mediating variable. Data analysis was performed using multiple linear regressions and Baron and Kenny’s method to test the mediating impact. The results indicate that all six independent variables significantly influence life insurance purchase behaviour. Furthermore, purchase intention was found to partially mediate the relationship for insurance literacy, attitude, subjective norms and perceived behavioural control, while exerting a full mediation effect for trust and risk perception. The findings suggest that insurance companies and policymakers should prioritise enhancing life insurance literacy and building trust to increase penetration. Tailored marketing strategies focusing on young adults and educated segments are recommended to expand the market reach and strengthen social security in the country.

Life insurance, purchase behaviour, purchase intention, mediating impact, Sri Lanka

Introduction

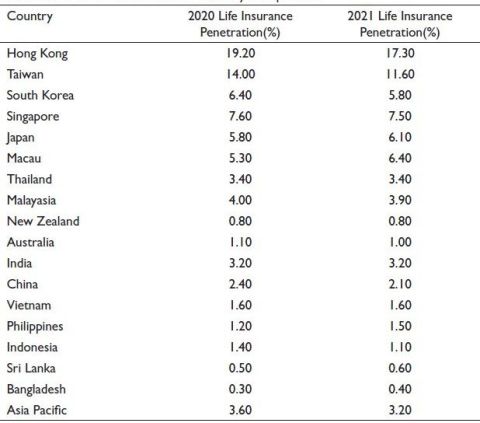

Insurance acts as a risk-transfer mechanism where individuals or organisations pay a premium to transfer uncertainty. The life insurance sector, a key part of insurance alongside general insurance, serves as a disciplined contractual saving method and a crucial source of long-term fund accumulation. To determine the use of insurance, one must first measure the performance of a country’s insurance sector. According to Chaudhary and Kaur (2016), developed countries have high insurance penetration rates, while developing countries have low rates. As a developing country, Sri Lanka has a low level of total insurance penetration as well as a low life insurance penetration rate, despite the benefits of life insurance. Further, it is highlighted in many articles as well. Table 1 illustrates the life insurance penetration rate in Sri Lanka compared with other countries, according to the Atlas Magazine, which was published on 24 May 2024.

Table 1. Life Insurance Penetration Country Comparison.

Source: From Table ‘Insurance penetration rate in Asia-Pacific’ (Atlas Magazine, 2024).

However, Sri Lanka has enjoyed an increasing real GDP growth rate after the COVID-19 pandemic. According to the formula that calculates the insurance penetration rate, increasing GDP causes an increase in the life insurance penetration rate. Nevertheless, the life insurance penetration rate has been reduced due to the decline in the growth rate of insurance premiums income after the COVID-19 pandemic, as indicated in Table 2. Additionally, with reference to the press release of the Insurance Regulatory Commission of Sri Lanka (IRCSL), they have partnered with the Department of Demography at the University of Colombo and conducted a comprehensive study on public confidence in insurance. Based on the findings, they have highlighted that overall confidence in insurance among the public was at an average level, with general insurance but not life insurance.

A low life insurance penetration rate leads to various disadvantages for a country. Therefore, it is imperative to investigate the factors contributing to low life insurance penetration and implement strategies to increase uptake. To address this issue, most researchers focus more on what factors affect low insurance penetration. Since insurance penetration is calculated using insurance premiums, it is essential to identify whether individuals purchase insurance policies or not. Therefore, the research has focused on individuals’ purchase behaviour of life insurance policies. Insurance literacy (Mai et al., 2020; Masud et al., 2021; Md et al., 2017; Omar, 2007), attitudes (Luciano et al., 2015), subjective norms (Echchabi & Aziz, 2012a; Lada et al., 2009), trust (Ling et al., 2010; Omar, 2007; Panigrahi et al., 2018), risk perception (Arun et al., 2012; Md Husin & Ab Rahman, 2016) and perceived behavioural control (Md Husin & Ab Rahman, 2016; Masud et al., 2021; Taylor & Todd, 1995) have been identified as factors that might be influencing the purchase behaviour of individuals. Based on the existing body of knowledge relating to the Sri Lankan context, researchers have identified that insurance literacy, attitudes, trust and risk perception are some factors that influence the Sri Lankan life insurance purchasing behaviour of people. But still, there are a limited number of research articles that have been done under this topic. It is also uncertain if factors like subjective norms and perceived behavioural control, which influence insurance purchases in other countries, have the same effect on people in Sri Lanka.

Accordingly, this study intends to uncover ‘What Factors Affect Purchase Behaviour of Life Insurance in Sri Lanka?’ To determine the purchase behaviour of individuals, purchase intention also has a direct impact (Muda et al., 2016). Therefore, researchers expect to investigate whether purchase intention mediates the relationship between factors that have been identified and the purchase behaviour.

Table 2. Life Insurance Penetration Level in Sri Lanka 2018–2022, According to the Insurance Regulatory Commission of Sri Lanka (IRSCL).

Source: From Table ‘Premium Income and Penetration’ (Insurance Regulatory Commission of Sri Lanka, 2022).

Based on the research questions, the researchers have developed the following research objectives:

They will provide significant insights for insurance companies, policymakers and future researchers in Sri Lanka, aiding decision-making related to life insurance uptake.

Literature Review

The literature review for this study is based on two fundamental behavioural theories: Ajzen’s (1991) Theory of Planned Behaviour (TPB) and Fishbein and Ajzen’s (1975) Theory of Reasoned Action (TRA). TPB describes behaviour in terms of intention, which is influenced by three important components: attitude towards the behaviour, subjective norms and perceived behavioural control (Ajzen, 1991; Echchabi & Aziz, 2012a; Fishbein & Ajzen, 1975). According to TRA, an individual’s attitude and the influence of significant individuals impact their intentions, in other words, subjective norms (Lada et al., 2009). These frameworks are commonly used to study financial decision-making behaviours, such as the purchase of life insurance. Based on these theories, the study finds six critical variables: insurance literacy, attitudes, subjective norms, trust, risk perception and perceived behavioural control as primary influences on buy intention, which in turn influences purchase behaviour.

Based on empirical studies, key factors that are related to the intention to purchase insurance policies have been identified. Moreover, the findings for six critical variables examine their relevance and impact within both global and South Asian contexts.

Insurance: This is a financial mechanism designed to mitigate the negative financial impact of uncertain events or potential losses. It acts as a protective agreement against unforeseen circumstances (Zou & Adams, 2006). Life insurance, specifically, is a fortuity contract contingent on an unanticipated event outside the insured’s control (Blunden & Thirlwell, 2013). Consumer behaviour in life insurance is intricate, encompassing decision-making processes and influencing factors (Dodamgoda & Canagasabey, 2019).

Insurance purchase behaviour: This involves customers’ decisions and the reasoning behind their choices when acquiring insurance (Schoultz et al., 2022). It is a critical consumer decision, encompassing actions involved in acquiring, utilising and disposing of goods and services, alongside the underlying decision-making processes (Aliyu et al., 2014). Research consistently shows a direct link between purchase intention and actual behaviour. A household’s perception of life insurance is a key determinant (Schoultz et al., 2022), and their purchasing tendency influences the behaviour (Masud et al., 2021).

Insurance literacy: Based on the global context, informed consumption requires understanding policy terms, comparing insurers and recognising rights and responsibilities (Tennyson, 2011). Customer confidence in insurance decisions is linked to insurance literacy (Tennyson, 2011).

According to the South Asian Context, a significant portion of the community lacks awareness of life insurance benefits (Farooq et al., 2015), posing a barrier to purchase. Low awareness of benefits is prevalent among Malaysians (Masud et al., 2021). Awareness (insurance literacy) has a positive relationship with purchase intention (Arun et al., 2012; Md et al., 2017; Omar, 2007) and directly influences attitude towards life insurance purchase (Md Husin & Ab Rahman, 2016).

H1: There is a significant impact of insurance literacy on life insurance purchase behaviour in Sri Lanka.

H2: There is a significant impact of insurance literacy on life insurance purchase intention in Sri Lanka.

H3: Purchase intention mediates the relationship between insurance literacy and purchase behaviour.

Attitudes: An attitude is an individual’s favourable or unfavourable response to an object, person or event, which helps predict behaviour (Ajzen, 1991). Under the global context, attitude significantly impacts the intention to purchase insurance (Md Husin & Ab Rahman, 2016). Awareness directly influences attitudes towards purchasing life insurance (Md Husin & Ab Rahman, 2016), supporting the idea that attitudes shape behaviour. Attitude is a crucial factor in determining purchase intention, with a significant relationship between attitude and behavioural intention (Jung et al., 2016; Phau et al., 2009). Based on the South Asian context, attitudes vary in risky situations, with attitude being a significant positive predictor of behaviour. Malaysians often exhibit unfavourable attitudes towards life insurance, regardless of its value (Masud et al., 2021). Attitude is significantly connected to behavioural intention (Jung et al., 2016), and factors like awareness, purchasing capacity and trust influence buyers’ attitudes (Valentina-Daniela & Gheorghe, 2015).

H4: There is a significant impact of attitudes on life insurance purchase behaviour in Sri Lanka.

H5: There is a significant impact of attitudes on life insurance purchase intention in Sri Lanka.

H6: Purchase intention mediates the relationship between attitude and purchase behaviour.

Subjective norms: They are the perceived social pressure from influential others to engage or not engage in a particular behaviour (Chen & Yang, 2018). Based on the global context, subjective norms are a significant predictor of an individual’s intention to behave in a specific way, particularly when purchasing financial products (Echchabi & Aziz, 2012b; Hasbullah et al., 2016) or life insurance (Md Husin & Ab Rahman, 2016). They significantly impact the intention to purchase insurance policies (Md Husin & Ab Rahman, 2016; Syed et al., 2012). When considering the South Asian Context, attitude and subjective norms have a more significant positive impact on consumer purchase intention towards life insurance. Subjective norms are crucial to an individual’s intention to behave in a particular manner, such as making a purchase (Echchabi & Aziz, 2012b; Lada et al., 2009).

H7: There is a significant impact of subjective norms on life insurance purchase behaviour in Sri Lanka.

H8: There is a significant impact of subjective norms on life insurance purchase intention in Sri Lanka.

H9: Purchase intention mediates the relationship between subjective norms and purchase behaviour.

Trust: It refers to the depth and certainty of feelings based on uncertain evidence, or a party’s willingness to accept another’s actions based on the expectation of proper execution, regardless of monitoring capacity (Tingchi Liu et al., 2013). Global context highlights that trust is a crucial factor influencing purchase decisions (Chen & Barnes, 2007; Hasbullah et al., 2016), highlighting its importance in insurance purchase intention. Based on the South Asian context, the public often lacks trust in insurance firms to repay premiums upon expiry (Farooq et al., 2015). Trust significantly influences individual behaviours and perceptions.

H10: There is a significant impact of trust on life insurance purchase behaviour in Sri Lanka.

H11: There is a significant impact of trust on life insurance purchase intention in Sri Lanka.

H12: Purchase intention mediates the relationship between trust and purchase behaviour.

Risk perception: This involves assessing the perceived severity and probability of a threatening event (Alfiero et al., 2022). According to the global context, perceived risk positively impacts the intention to buy insurance (Alfiero et al., 2022). People’s perception of risk significantly influences their decision to purchase insurance. The South Asian context highlights that risk aversion influences the willingness to purchase life insurance. Risk-averse individuals tend to prefer lower risk and predictable outcomes (Ofoghi & Farsangi, 2013), making them more likely to obtain life insurance (Masud et al., 2021). Risk perception is crucial for encouraging life insurance purchases (Omar, 2007), influenced by potential future risks and financial benefits. Higher perceived risk correlates with a greater willingness to purchase insurance, and awareness of involved risks increases purchase likelihood (Md Husin & Ab Rahman, 2016).

H13: There is a significant impact of risk perception on life insurance purchase behaviour in Sri Lanka.

H14: There is a significant impact of risk perception on life insurance purchase intention in Sri Lanka.

H15: Purchase intention mediates the relationship between risk perception and purchase behaviour.

Perceived behavioural control: This refers to an individual’s belief in their ability to perform a behaviour without external influence (Masud et al., 2021; Shih & Fang, 2004). It also encompasses an individual’s perception of the ease or difficulty of carrying out certain behaviours (Ajzen & Madden, 1986), reflecting self-efficacy, skills and resources (Shih & Fang, 2004; Taylor & Todd, 1995). Based on the global context, there is a significant relationship between perceived behavioural control and intention (Md Husin & Ab Rahman, 2016), and a positive correlation with insurance purchase intention (Md Husin & Ab Rahman, 2016). While some studies show a positive influence on purchase intention (Alfiero et al., 2022), its effect may vary depending on the insurance type.

H16: There is a significant impact of perceived behavioural control on life insurance purchase behaviour in Sri Lanka.

H17: There is a significant impact of perceived behavioural control on life insurance purchase intention in Sri Lanka.

H18: Purchase intention mediates the relationship between perceived behavioural control and purchase behaviour.

The mediating effects of purchase intention signify a customer’s willingness to repurchase a product they deem worthwhile, or a preference to buy due to perceived need or attitude. It is the ultimate decision point for consumers and a significant predictor of actual purchase behaviour (Mai et al., 2020). It influences life insurance purchase behaviour and mediates between explanatory variables and purchase behaviour (Alfiero et al., 2022; Masud et al., 2021).

H19: There is a significant impact of purchase intention on purchase behaviour in Sri Lanka.

These studies highlight the complicated relationship of psychological, social and informational elements in life insurance decisions. This study expands on these findings to investigate how these variables influence purchase behaviour in the Sri Lankan context, with purchase intention acting as a mediating factor, as supported by Baron and Kenny’s mediation framework and validated in previous studies (Mai et al., 2020; Masud et al., 2021).

Research Methodology

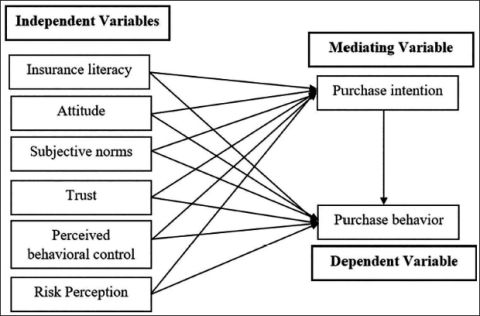

This study used a quantitative research approach to investigate the factors influencing life insurance buying behaviour in Sri Lanka. The study technique included a systematic questionnaire spread across all nine provinces in both online and printed modes, which allowed for the collection of a wide range of primary data. The sample was selected using a stratified random sampling method with a total sample size of 391 respondents. The sample size is consistent with the sample size suggested by Krejcie and Morgan’s table. The replies reflected views from a wide range of age groups, vocations and educational levels. Based on the TPB and the TRA, the study created a conceptual framework as given in Figure 1 with six independent variables: insurance literacy, attitudes, subjective norms, trust, risk perception and perceived behavioural control, and investigated the mediating role of purchase intention on purchase behaviour.

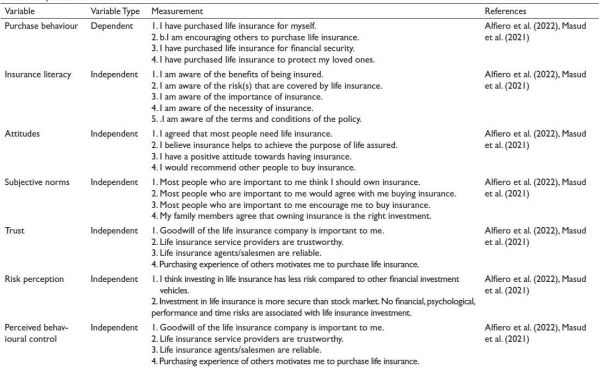

Table 3 includes operationalisation criteria and measurement methods for the study’s variables, aligning with the conceptual framework. The research questions were adapted from established literature to evaluate the independent, dependent and mediating variables. A five-point Likert scale was employed to measure the responses, with values ranging from 1 (strongly disagree) to 5 (strongly agree).

SPSS was used to analyse the data, which included descriptive statistics, correlation analysis, multiple linear regression and Baron and Kenny’s approach for investigating mediation effects. This technique offered a solid framework for evaluating the links between the fundamental concepts and providing practical insights into consumer behaviour in the life insurance industry.

Figure 1. Conceptual Framework.

Source: Authors’ construction based on literature survey.

Table 3. Operationalisation.

Results and Discussion

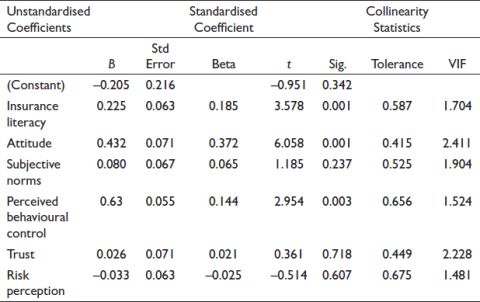

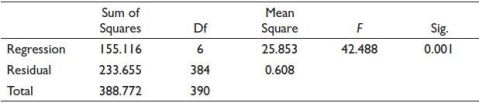

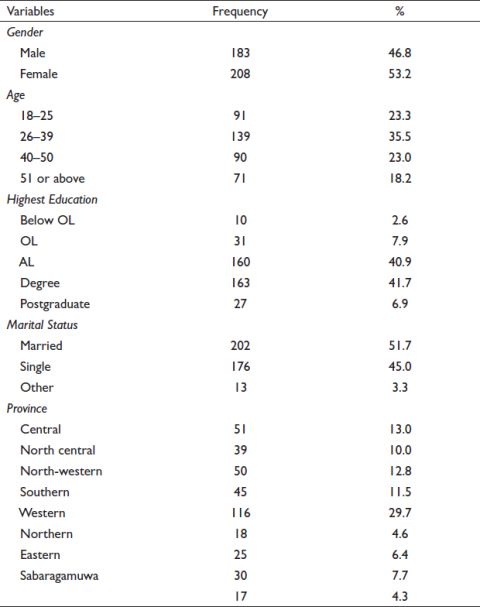

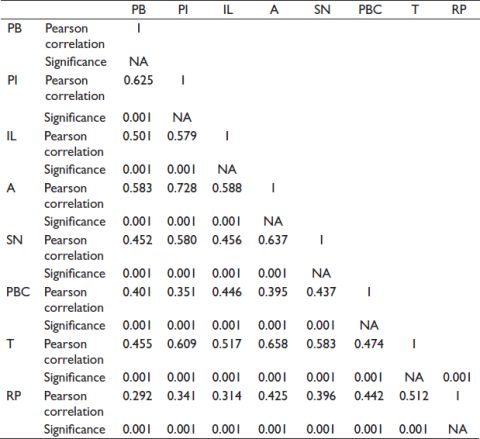

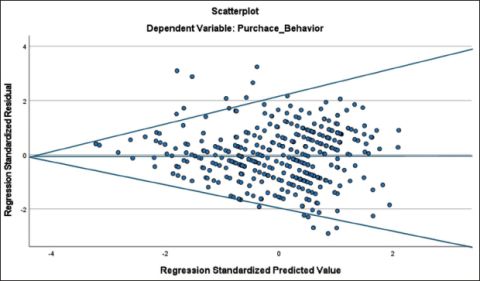

This section provides a comprehensive understanding of the analysis that was used to meet the ultimate objective of this study. Testing the reliability and validity of data makes the foundation for further analysis. Additionally, researchers have highlighted the normality of the data in different ways. According to the outcomes of the regression analysis, the analysis of variance (ANOVA) table is 1% significant, and that plays a critical role in the analysis. The profile of the respondents indicates a summary of 391 individual profile responses to the questionnaire survey (Annexure 1). Moreover, descriptive statistics emphasise the overview of all variables in this study. Correlation analysis considers the relationship between purchase behaviour (DV) and independent variables; except for risk perception (RP), there is 1% significant relationship (Annexure 2). However, there is a moderate positive relationship between risk perception and insurance purchase behaviour (Annexure 2). Under ordinary least squares (OLS) assumptions, the heteroscedasticity test shows that some residuals are lying outside the triangle-shaped lines. That means the variance of the residuals is constant (Annexure 3). According to the serial correlation test, model regression summary in the Annexure 4, the Durbin–Watsons value is 1.751. Since the model’s value is between 1.5 and 2.5 range, the model is residually independent. As per the multicollinearity test, the variance inflation factor (VIF) values of Annexure 5 show that all the variables do not have multicollinearity problems since all the VIF values are less than 5. Finally, the findings support the applicability of the TPB and the TRA in the Sri Lankan context while providing valuable insights into the dynamics of life insurance purchasing behaviour in Sri Lanka.

Regression Results

Multiple Linear Regression.

Multiple linear regression analysis was conducted on cross-sectional survey data collected from respondents using SPSS software to analyse and quantify the relationship between the study’s independent and dependent variables. This was done in order to determine whether the factors that have been identified are really affected by the purchasing of life insurance decisions of the general public in Sri Lanka.

R2 measures the model’s overall regression accuracy and the proportion of the dependent variable’s variance explained by the independent variables. R2 values should range from 0 to 1, inclusive. According to the model summary as given in Table 4, the coefficient of determination is 0.399. This means 39.9% of the dependent variable, purchase behaviour, has been explained by the model. Since it is more than 20%, the model can be applied.

The adjusted R2 value of the model is 0.390. There is no huge change between the R2 and the adjusted R2. Therefore, the researchers can conclude that there are no unnecessary independent variables in the model. When it comes to the multicorrelation, the value is 0.632. That means independent variables: insurance literacy, attitude, subjective norms, trust, risk perception and perceived behavioural control are jointly correlated with the dependent variable: purchase behaviour.

Table 4. Model Summary.

Notes: Dependent variable: Purchase behaviour; Predictors: (Constant), Risk perception, Insurance literacy, Subjective norms, Perceived behavioural control, Purchase intention, Trust, Attitude.

Table 5. Analysis of Variance (ANOVA) Test.

Note: Dependent variable: Purchase behaviour; b. Predictors: (Constant), Risk perception, Insurance literacy, Subjective norms, Perceived behavioural control, Purchase intention, Trust, Attitude.

According to the ANOVA table (Table 5), the model is statistically significant with a 1% significant level, which means all the independent variables jointly influence the dependent variable purchase behaviour. That is why this model is an appropriate model.

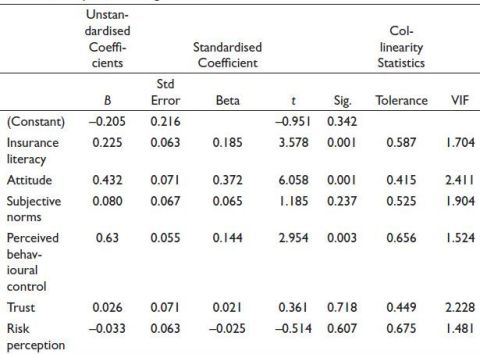

According to Table 6, the constant of the regression is negative 0.205. Insurance literacy and attitude have positive coefficients in the regression, and according to the p value, both variables are highly significant. Perceived behavioural control also has a positive coefficient and is significant. Similarly, subjective norms and trust have positive coefficients. Nevertheless, when it comes to the p values, both variables are not significant. However, the variable risk perception has a negative coefficient and it is not significant.

When it comes to the standard coefficient beta, the most dominant variable is attitude, scoring the highest value. Insurance literacy and perceived behavioural control, respectively, take second and third place when considering the standard coefficient beta. When management makes decisions, they need to pay attention to this order.

Hypothesis Testing

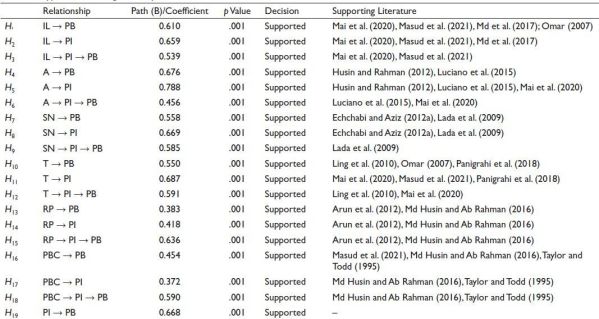

There are certain hypotheses that have been tested in this study. Table 7 shows the hypotheses that are used to carry out the research and the status of those hypotheses, whether they are supported or not supported.

Table 6. Multiple Linear Regression.

Mediating Analysis

The models that have been used for mediating analysis are as follows.

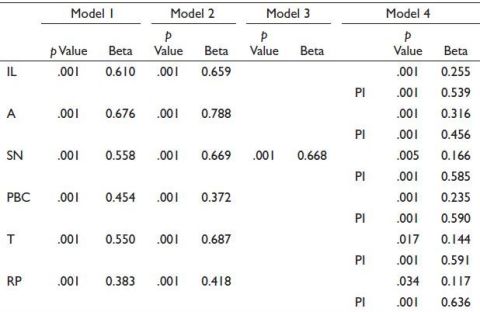

Researchers have analyzed the mediating effect of purchase intention by using the Baron and Kenny (1986) method. The results reported in Table 8 demonstrate that all the independent variables (IL, A, SN, PBC, T, RP) significantly influence the dependent variable (PB) according to model 1, and it is 1% significant. Model 2 represents all the independent variables (IL, A, SN, PBC, T, RP) that significantly influence the mediator (PI). Moreover, model 3 also supports this and the mediator (PI) has significantly influenced the dependent variable (PB).

Due to these 3 conditions are satisfied, it is shown that there is a mediating effect (Table 8). Therefore, final model 4 is analyzed by using independent variables (IL, A, SN, PBC, T, RP) and the mediator (PI) to the dependent variable (PB). According to the findings, insurance literacy (IL), attitude (A), and perceived behavioral control (PBC) along the mediator (PI) were 1% significant with the dependent variable (PB), while subjective norms (SN) were 5% significant with the dependent variable (PB). It reveals that purchase intention (PI) partially mediates the relationship between these variables and the dependent variable (PB) due to the direct relationship between insurance literacy (IL), attitude (A), perceived behavioral control (PBC), subjective norms (SN) and the dependent variable (PB) even after accounting for purchase intention. However, there is a full mediation effect between trust (T), risk perception (RP), and the dependent variable (PB) due to these independent variables no longer influence the purchase behavior (PB) after the mediator has been controlled.

Table 7. Hypotheses Testing Summary.

Table 8. Mediating Analysis Models.

Implications, Limitations and Suggestions for Future Research

This research highlights both the theoretical and practical implications of its findings on life insurance purchase behaviour. Theoretically, the study reinforces the validity of the TPB and the TRA by demonstrating that attitude, subjective norms and perceived behavioural control are significant predictors of purchasing life insurance. IRCSL has consistently emphasised the importance of consumer education to boost insurance penetration. IRCSL’s Annual Report 2021 highlighted that they empower public awareness through consumer education activities through print, electronic and social media. This included their rights, the importance of insurance and how to select suitable products. Additionally, they have mandated that all insurance policies must be available in all three official languages to reduce public confusion and build confidence. But in practicality, the research suggests that policymakers and insurance companies should prioritise factors like attitude, insurance literacy and subjective norms to increase life insurance penetration. This can be achieved through awareness campaigns, highlighting positive experiences, addressing misconceptions, and offering diverse and accessible product options.

Despite its contributions, the study acknowledges several limitations. The lack of prior research covering all provinces in Sri Lanka necessitated reliance on studies from other countries. Furthermore, the study’s focus on only six quantitative factors and its neglect of qualitative influences may provide an incomplete picture of the drivers behind life insurance purchase decisions. The use of questionnaires also introduces the potential for socially desirable responses, which could impact the accuracy of the data.

To build upon this research, future studies are recommended to broaden the scope by investigating additional factors such as cultural influences, socio-economic conditions, product innovations and qualitative characteristics. Researchers could also explore more complex interrelationships between variables and examine the impact of digital platforms and digital literacy on life insurance purchase behaviour (Annexure 3). Expanding the target audience to include insurance companies and policymakers could provide a more comprehensive understanding of the factors influencing life insurance adoption in Sri Lanka from multiple perspectives.

Conclusion

This research provides a comprehensive analysis of the factors affecting life insurance purchase behaviour in Sri Lanka. The study confirms the significant influence of insurance literacy, attitude, subjective norms, trust, risk perception and perceived behavioural control on purchase behaviour, with purchase intention playing a mediating role. These findings have important implications for the Sri Lankan insurance industry and future research directions.

Ajzen, I. (1991). The theory of planned behavior. Organizational Behavior and Human Decision Processes, 50(2), 179–211.

Ajzen, I., & Madden, T. J. (1986). Prediction of goal-directed behavior: Attitudes, intentions, and perceived behavioral control. Journal of Experimental Social Psychology, 22(5), 453–474.

Alfiero, S., Battisti, E., & Ηadjielias, E. (2022). Black box technology, usage-based insurance, and prediction of purchase behavior: Evidence from the auto insurance sector. Technological Forecasting and Social Change, 183, 121896.

Aliyu, A. A., Bello, M. U., Kasim, R., & Martin, D. (2014). Positivist and non-positivist paradigm in social science research: Conflicting paradigms or perfect partners. Journal of Management and Sustainability, 4(3), 79.

Arun, T., Bendig, M., & Arun, S. (2012). Bequest motives and determinants of micro life insurance in Sri Lanka. World Development, 40(8), 1700–1711.

Atlas Magazine. (n.d.). Insurance penetration rate in Asia-Pacific. https://www.atlas-mag.net/en/category/tags/pays/insurance-penetration-rate-in-asia-pacific

Blunden, T., & Thirlwell, J. (2013). Mastering operational risk: A practical guide to understanding operational risk and how to manage it. Pearson UK.

Chaudhary, S., & Kaur, J. (2016). Consumer perception regarding life insurance policies: A factor analytical approach. Pacific Business Review International, 9(6), 52–61.

Chen, L., & Yang, X. (2018). Using EPPM to evaluate the effectiveness of fear appeal messages across different media outlets to increase the intention of breast self-examination among Chinese women. Health Communication, 34(11), 1369–1376.

Chen, Y. H., & Barnes, S. (2007). Initial trust and online buyer behaviour. Industrial Management & Data Systems, 107(1), 21–36.

Dodamgoda, N., & Canagasabey, D. (2019). Factors driving the purchase of life insurance among millennials in Sri Lanka. International Journal of Business Marketing and Management (IJBMM), 4(5), 49–61.

Echchabi, A., & Aziz, H. A. (2012a). Empirical investigation of customers’ perception and adoption towards Islamic banking services in Morocco. Middle-East Journal of Scientific Research, 12(6), 849–858.

Echchabi, A., & Aziz, H. A. (2012b). The relationship between religiosity and customers’ adoption of Islamic banking services in Morocco. Oman Chapter of Arabian Journal of Business and Management Review, 34(967), 1–6.

Farooq, M., Roman, M., Mohsin, N., Riaz, F., & Anwar, H. N. (2015). People’s attitude towards life insurance in Pakistan. Mediterranean Journal of Social Sciences, 6(3).

Fishbein, M., & Ajzen, I. (1975). Belief, attitude, intention, and behavior: An introduction to theory and research. Addison-Wesley.

Hasbullah, N. A., Osman, A., Abdullah, S., Salahuddin, S. N., Ramlee, N. F., & Soha, H. M. (2016). The relationship of attitude, subjective norm and website usability on consumer intention to purchase online: An evidence of Malaysian youth. Procedia Economics and Finance, 35, 493–502.

Insurance Regulatory Commission of Sri Lanka. (2022). Statistical review. https://ircsl.gov.lk/wp-content/uploads/2023/09/Statistical-Review-2022-final-15-09-2023.pdf

Jung, J., Shim, S. W., Jin, H. S., & Khang, H. (2016). Factors affecting attitudes and behavioural intention towards social networking advertising: A case of Facebook users in South Korea. International Journal of Advertising, 35(2), 248–265.

Lada, S., Harvey Tanakinjal, G., & Amin, H. (2009). Predicting intention to choose halal products using theory of reasoned action. International Journal of Islamic and Middle Eastern Finance and Management, 2(1), 66–76.

Ling, K. C., Chai, L. T., & Piew, T. H. (2010). The effects of shopping orientations, online trust and prior online purchase experience toward customers’ online purchase intention. International Business Research, 3(3), 63.

Luciano, E., Outreville, J. F., & Rossi, M. (2015). Life insurance demand: Evidence from Italian households; a micro-economic view and gender issue. SSRN Electronic Journal.

Mai, T., Nguyen, T., Vu, L., Bui, V., & Do, D. (2020). A study on behaviors of purchasing life insurance in Vietnam. Management Science Letters, 10(8), 1693–1700.

Masud, M. M., Ahsan, M. R., Ismail, N. A., & Rana, M. S. (2021). The underlying drivers of household purchase behaviour of life insurance. Society and Business Review, 16(3), 442–458.

Md Husin, M., & Ab Rahman, A. (2016). Predicting intention to participate in family takaful scheme using decomposed theory of planned behaviour. International Journal of Social Economics, 43(12), 1351–1366.

Md, N., Shahedul, A. S. M., & Md, F. R. (2017). Measuring people’s attitude towards the life insurance in Rangpur City Corporation in Bangladesh. International Journal of Economics &Management Sciences, 6(2).

Muda, M., Mohd, R., & Hassan, S. (2016). Online purchase behavior of generation Y in Malaysia. Procedia Economics and Finance, 37, 292–298.

Ofoghi, R., & Farsangi, R. H. (2013). The effect of insurance knowledge on the insurance demand: The case study of auto insurance. Technical Journal of Engineering and Applied Sciences, 3(23), 3356–3364.

Omar, O. E. (2007). The retailing of life insurance in Nigeria: An assessment of consumers’ attitudes. The Journal of Retail Marketing Management Research.

Panigrahi, S., Azizan, N. A., & Waris, M. (2018). Investigating the empirical relationship between service quality, trust, satisfaction, and intention of customers purchasing life insurance products. Indian Journal of Marketing, 1, 41–47.

Phau, I., Sequeira, M., & Dix, S. (2009). Consumers’ willingness to knowingly purchase counterfeit products. Direct Marketing: An International Journal, 3(4), 262–281.

Schoultz, C., Spetz, E., & Pettersson, I. (2022). Psychological factors impacting the consumer buying behavior: A study investigating how the psychological factors impact the cognitive decision-making process within the make-up industry [Bachelor’s thesis, Jönköping University].

Shih, Y. Y., & Fang, K. (2004). The use of a decomposed theory of planned behavior to study Internet banking in Taiwan. Internet Research, 14(3), 213–223.

Taylor, S., & Todd, P. A. (1995). Understanding information technology usage: A test of competing models. Information Systems Research, 6(2), 144–176.

Tennyson, S. (2011). Consumers' insurance literacy: Evidence from survey data. Financial Services Review, 20(3), 165–179.

Tingchi Liu, M., Brock, J. L., Cheng Shi, G., Chu, R., & Tseng, T. H. (2013). Perceived benefits, perceived risk, and trust: Influences on consumers’ group buying behaviour. Asia Pacific Journal of Marketing and Logistics, 25(2), 225–248.

Valentina-Daniela, C., & Gheorghe, O. (2015). Potential buyers’ attitude towards life insurance services. Procedia Economics and Finance, 32, 1083–1087.

Zou, H., & Adams, M. B. (2006). The corporate purchase of property insurance: Chinese evidence. Journal of Financial Intermediation, 15(2), 165–196.

Annexure 1: Profile of the Respondents

Annexure 2: Correlation Analysis

Annexure 3: Heteroscedasticity

Annexure 4: Serial Correlation

Annexure 5: Multicollinearity